Food Processing Skills Canada (FPSC), is pleased to present this report to the food and beverage processing industry, government decision makers and other stakeholders.

This report stands as a resource for all. It details who the industry is, where it could go, and what’s standing in its way. Producing this report in these challenging times has been a moving target. The world has changed and it’s hard to know how history will look back on this time. A tectonic shift in every sector, and in everyday life, has occurred virtually simultaneously across the entire globe. This report outlines what we observe to be the immediate economic and financial consequences of the COVID-19 global pandemic. However, according to our experts, the medium and longer-term impacts of COVID-19 on Canadian businesses cannot be fully estimated.

employers facing recruitment and retention challenges.

The hiring requirement for the industry by 2025

people employed in the food and beverage processing industry.

businesses located across the country.

“91% of food and beverage processing businesses employ less than 100 people.”

Canada’s food and beverage processors are the link between farms and the sea and our tables. We transform Canada’s agricultural and seafood commodities into a wide array of products for consumers or further processing. To put a finer point on it; almost every food or beverage product we consume is processed in some manner. This is a large, high value industry that touches every Canadian. It is also an industry at the crossroad to greatness.

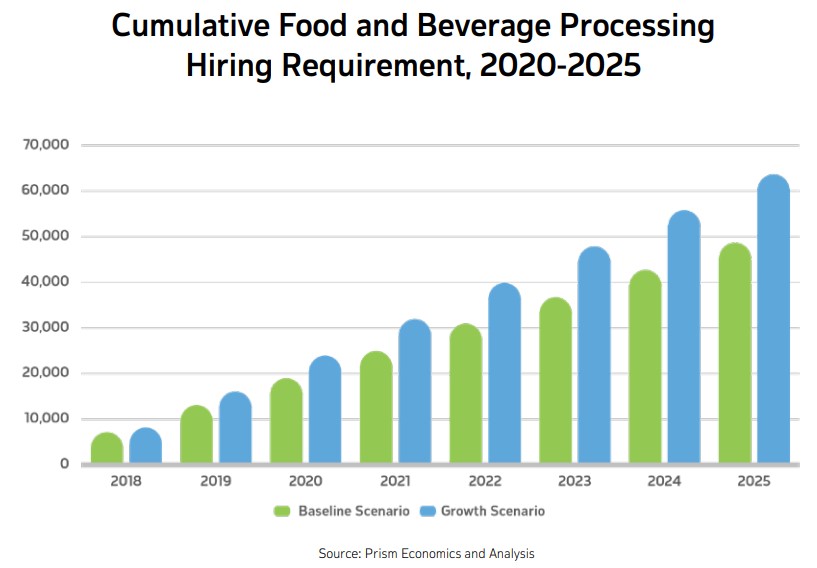

The hiring requirement for the industry over the 2020-2025 period in the “the baseline scenario” is estimated at about 35,000 (or 12% of the industry’s workforce in 2020).

In “the growth scenario” the total hiring requirement rises to 56,000 workers equivalent to 20% of the industry’s 2020 workforce and an additional 21,000 workers over the baseline forecast.

If those figures aren’t startling enough, this report illustrates that we’re starting from a critical labour shortage deficit today, and its coming at a great cost.

FPSC conducted this labour market information study to deliver detailed industry data highlighting tensions and opportunities, as well as actionable recommendations, to employers, government decision makers and other stakeholders. This report presents the findings of robust research drawing on numerous credible methodologies, including information on industry trends, labour trends, demographics, and key results from several surveys. Information is provided for the sector as a whole, as well as for the 11 sub-sectors that comprise it.

This report comes at a time when the sector is facing a combination of unprecedented opportunities, and also challenges. In addition, it is fair to say that the salience of this report has increased in light of the COVID-19 global pandemic.

We designed this report to flow from the general to the specific, with the latter based on meaningful input of the many hundreds of industry employers and labour market participants.This report comes at a time when the sector is facing a combination of unprecedented opportunities, and also challenges. In addition, it is fair to say that the salience of this report has increased in light of the COVID-19 global pandemic.

The report begins with a profile of the Canadian food and beverage processing industry, including its contribution to the economy, sub-sectors, geographical distribution, opportunities for growth and barriers to growth. This is followed by an examination of key trends shaping the future of the sector, ranging from consumer preferences, climate change and the advent of Industry 4.0.

Then, we move to an analysis of major labour trends in the sector, including a projection of labour requirements to 2025 based on two different growth scenarios. Included here is a profile of the sector’s labour force by key sociodemographic characteristics, such as age, gender, location, as well as a profile of major occupations.

The wide range of human resource issues faced by the sector are examined, as well as some of the key approaches that have been implemented by employers in response. Most of this information comes from three surveys, including one of employers and two of labour market participants. The third section assesses the impact that the COVID-19 pandemic has had on the industry. The end of the report is dedicated to conclusions and actionable recommendations.

Economic analysis estimates that a single unfilled position in the food and beverage processing industry could cost businesses as much as $190 per day in lost net revenue. That may not seem like much, but when you aggregate it over the entire sector, losses from job vacancies could total up to an estimated $8.5M in net revenue per day. If this is not addressed the $8.5M per day becomes $3.1B annually.

These figures underscore that this is not a human resource issue alone, it’s actually the most critical business challenge for the industry. As this report reveals, labour availability is the top overall business challenge, ahead of coping with regulations, implementing technology and meeting customer preference.

7 in 10 employers report facing recruitment and retention challenges. Most of these employers describe the problem as persistent and on-going. The evidence also suggests that recruitment and retention problems have worsened over the past year.

How then can the industry “get its house in order” and address the most critical challenges employers face? Indeed, that is the purpose of this report. To outline the conditions that exist and deliver actionable recommendations for employers and governments.

This report shines a light on the challenges we face in recruiting, skills training and retaining qualified workers. It discusses the impact of integrating Industry 4.0 production processes and the effect it could have on reducing the hiring burden. We also explore the challenges we have to competitiveness in the industry.

We have included a detailed analysis of sector trends such as evolving consumer preferences, consolidating regulatory frameworks, cannabis edibles and infused beverages, and climate change that employers and governments alike should appreciate. The report also explores perceptions of the industry and impact on preferences.

To give employers and other stakeholders a sense of the overall industry dynamic, this report profiles jobs, how individuals are paid, including comparisons with other manufacturing sectors, and unionization across the sectors.

We take a critical look inside food and beverage processor businesses – from business priorities to human resources. With labour constraints and the need for appropriately skilled people, this report also provides guidance to employers on data-driven best practices. Specifically, we look at human resource challenges, access to immigration programs, employer recruitment and retention strategies, methods of outreach and communications, and employee benefits and other incentives.

There is also a specific analysis of studies that assess five generations in the workplace and identify underrepresented groups in the industry who are most interested in employment. The analysis is rounded out with a comprehensive review on building a skills foundation to meet the needs of the sector.

This report calls on employers, industry associations, government, and educational and research institutions to be nimble and take heed of the valuable lessons we have learned so far in this global pandemic. The research also demonstrates that with a willingness to explore new opportunities and an enthusiasm to embrace change, we can successfully reach the next great chapter of our industry. An industry that feeds Canada and the world, and is at the crossroad to greatness.

The information presented in this report was gathered from a wide variety of sources, including secondary and primary research. Each method was carefully selected to meet the study objectives. The methods complement each other so as to provide a 360-degree view of the industry across a range of key issues. Through the use of surveys and exhaustive reviews of labour market statistics and other data (e.g., relevant post-secondary education programs across Canada), the report goes into depth on several facets, including the industry’s initial response to the COVID-19 pandemic.

Each source is described in the table below.

The food and beverage processing industry with its more than 7,600 businesses directly employs over 280,000 people accounting for almost 1 in 5 of all manufacturing jobs in Canada. The COVID-19 global pandemic has also clearly shown the industry’s great strategic importance.

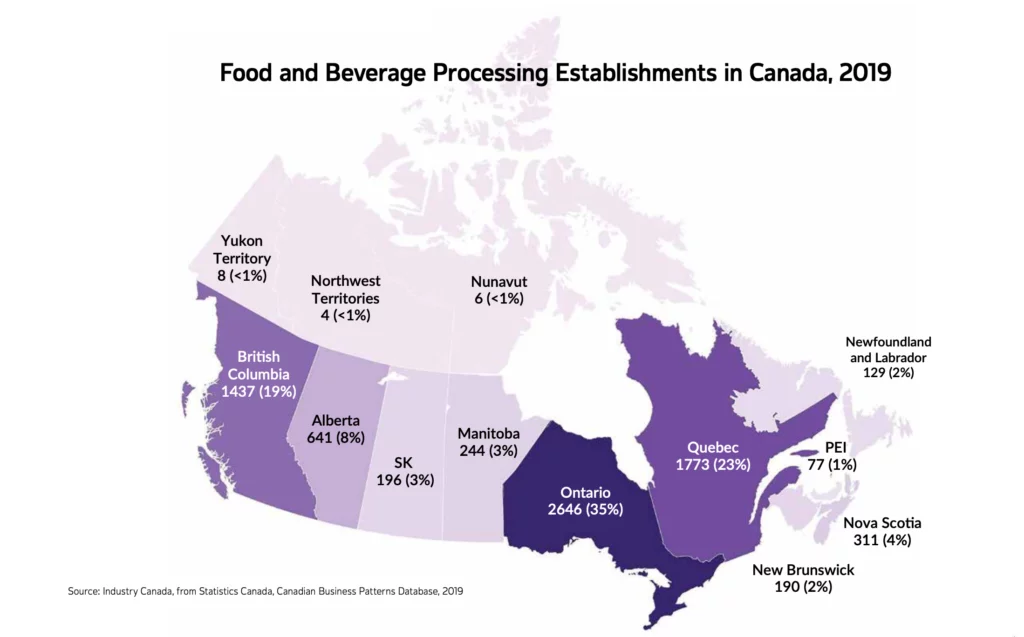

The industry is made up of 11 sub-sectors, with Meat Product Processing being the largest and Cannabis Product Manufacturing being the newest. Ontario, Quebec, and BC are home to three-quarters of the industry’s businesses.

The industry is dominated by small or medium-sized businesses, with fully 91% of businesses employing less than 100 people.

The growth target the Agri-Food Table has set for Canadian agricultural, agri-food and seafood exports to reach.

The increase in exports of Canadian processed food and beverage products between 2016 and 2020.

The percentage the global demand for food is expected to rise between 2009 and 2050.

Almost every food or beverage product we consume is processed in some manner.

The food and beverage processing sector is the link between farms, or the sea, and our tables, transforming Canada’s agricultural and seafood commodities into a wide array of products for consumers or further processing.

Below, we describe the size and nature of the food and beverage processing sector and delineate its global competitiveness. We also highlight opportunities for domestic and international growth, as well as discuss the labour market implications of sector growth.

Overall, we see that the industry is a major contributor to the Canadian economy. It also has significant growth potential, especially when compared to other sectors of manufacturing. The ambitious targets set for the industry reflect its potential. We also note that the COVID-19 pandemic has illustrated the strategic importance of food and beverage processors, and of the food supply chain more broadly.

However, it is critical to note that optimal industry growth can only happen with the right conditions. The last part of this chapter highlights the actions proposed by the Agri-Food Table for strengthening the Canadian agri-food sector.

The role of trade agreements, including interprovincial trade, are also key to sector growth.

"The food and beverage processing sector has significant growth potential, especially when compared to other sectors of manufacturing."

Size matters, but as the COVID-19 global pandemic has revealed – the sector is also of great strategic importance7

We define the food and beverage processing sector as those businesses engaged in Food Manufacturing (NAICS8 Code 311), Beverage Manufacturing (NAICS 3121) and Cannabis Product Manufacturing (NAICS 3123), which includes Cannabis edibles and infused beverages.

Food and beverage processing is the transformation of agricultural products into food or beverages, or of one form of food or beverage into other forms for consumption by humans or animals:

The definition of what constitutes a “processed” food or beverage is wide and encompassing.

In 2020, there were over 7,600 food and beverage processing businesses operating in the sector that employed at least one person, which adds up to a total workforce of more than 280,000. The vast majority of these establishments are small or medium-sized businesses9, with roughly 91 per cent of food and beverage processors in Canada having fewer than 100 paid employees10. Although food and beverage processing businesses are significant sources of employment in every province and territory, they are mostly concentrated in Ontario, Quebec and British Columbia. In these provinces, employers have access to large pools of labour and are close to consumers and their products, both in Canada and the United States (the sector’s largest export market).11

Meat Product Manufacturing was the sub-sector with the largest workforce in 2020, employing 65,113 people, followed by Bakeries and Tortilla Manufacturing (46,691), Beverage Manufacturing (42,094) and Other Food Manufacturing (35,543). Cannabis Product Manufacturing had the smallest workforce (2,700), while Grain and Oilseed Milling employed 8,722 people.12

Other Food Manufacturing (NAICS 3119) is an outlier within the food and beverage processing spectrum. This sub-sector represents over 40% of all the industry’s indeterminate businesses and covers the widest range of products of any sub-sector, it resembles the kitchen drawer with all of the odds and ends. This is further complicated by the fact many of the processors also manufacture products in one of the other 10 food

and beverage processing sub-sectors. This presents a challenge in understanding and accurately partitioning units of analyses such as facilities or employees according to sub-sectors given the potential overlapping sub-sectors as currently defined within the other foods category. Understanding the structure of the Other Food Manufacturing sub-sector in detail will contribute to improved outcomes and labour market information for the industry. It will limit the risk associated with the potential overlap such as double counting and understanding skills and HR requirements in having employees work across multiple sub-sectors.

Within Other Food Manufacturing there is a catch all subcategory called All Other Food Manufacturing, which is where the majority of new products get placed. As such, it is difficult to get an idea of the real drivers of growth within the sector as there is no effective

way to separate out economic and labour information. There are five subcategories within Other Food Manufacturing.

"Other Food Manufacturing resembles the kitchen drawer with all of the odds and ends, since it covers the widest range of products of any sub-sector."

Overview: This subcategory comprises establishments primarily engaged in salting, roasting, drying, cooking or canning nuts; processing grains or seeds into snacks; manufacturing peanut/nut butter; or, manufacturing potato chips, corn chips, popped popcorn, hard pretzels, pork rinds and similar snacks.

Overview: This subcategory comprises establishments primarily engaged in manufacturing soft drink concentrates and syrup, and related products for soda fountain use or for making soft drinks.

Overview: This subcategory comprises establishments primarily engaged in roasting coffee; manufacturing coffee and tea extracts and concentrates, including instant and freeze dried; blending tea; or, manufacturing herbal tea. Establishments primarily engaged

in manufacturing coffee and tea substitutes are included.

Overview: This subcategory comprises establishments primarily engaged in manufacturing dressings and seasonings.

Overview: This subcategory manufactures perishable prepared foods such as sandwiches, prepared meals and peeled or cut vegetables. Companies in the industry also use dried and dehydrated ingredients to manufacture dessert mixes, flavouring powders and processed eggs.

In 2018, All Other Food Manufacturing accounted for over 50% of the Other Food Manufacturing workforce, 65% of employers and nearly 70% of indeterminate businesses. This makes it incredibly difficult to determine where the growth in the sector is actually coming from.

Given this sub-sector’s size, diversity, and growth indicators, it is likely that many of the main drivers of the overall industry are linked to the issues and characteristics of this sub-sector. As a result, it is crucial to form a comprehensive understanding of the Other Food

Manufacturing sub-sector to develop valid and reliable knowledge and predictions for the industry

"In 2018, All Other Food Manufacturing accounted for over 50% of the Other Food Manufacturing workforce, 65% of employers and nearly 70% of indeterminate businesses."

As big as the industry is today, there is tremendous potential for it to become much bigger as the world demand for food more than doubles by 2050 and consumers demand new and innovative products.

To ensure that Canada is at the forefront of this rapidly growing sector at home and abroad, Canadian food and beverage processors must be able to recruit tens of thousands of new workers between now and 2025, as well as equip them with an increasingly diverse range of skills and knowledge.

In 2017, the Advisory Council on Economic Growth13 identified Canada’s agriculture and food sector as one of eight sectors with untapped potential and significant global growth prospects. The Council noted that, although the sector accounts for an impressive share of Canada’s GDP and is a major exporter of agricultural and agri-food products, Canada still ranks behind countries such as the Netherlands and Brazil. The Council challenged

the government and industry to work together “to unleash the sector’s full potential,”14 and set an ambitious target of increasing Canada’s agricultural and agri-food exports by US$30 billion over the next five to 10 years. The Council proposed that value-added agri-food exports should account for the bulk of these gains, doubling Canada’s share of world agri-food exports (to 5.6 per cent), with agricultural exports increasing to eight per cent of the

global total (from the current 5.7 per cent).15

This call was echoed by the Report of Canada’s Economic Strategy Tables: Agri-Food,16 (referred to in this report as “AgriFood Table”) which identified huge opportunities for Canada to build on its global reputation as a supplier of safe and highquality products, and in particular, to supply the growing demand around the world for protein.17 The Agri-Food Table set even more ambitious growth targets than those from the Advisory Council

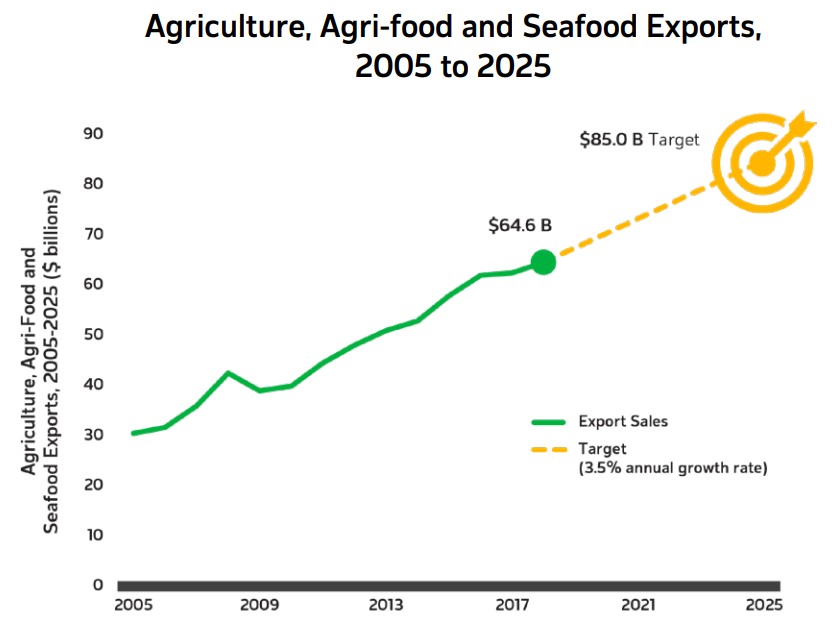

or the federal government,18 calling for Canadian agricultural, agri-food and seafood exports to reach $85 billion by 2025, a 32 per cent increase from 2017 levels.19

Since 2002, the food and beverage processing industry has vastly outperformed

Canadian manufacturing overall.

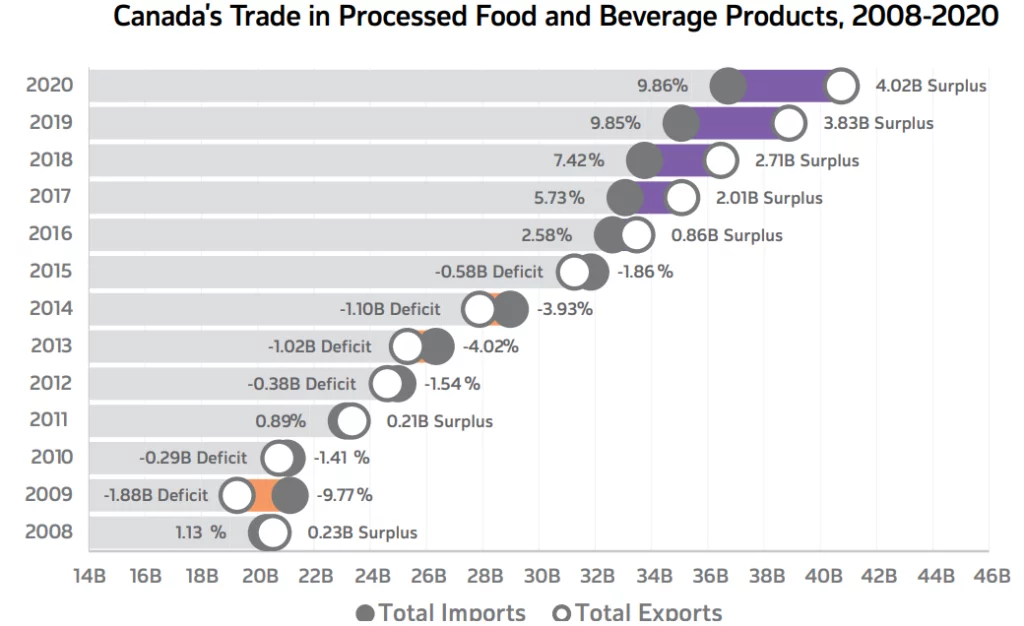

Exports of Canadian processed food and beverage products increased by over 22% between 2016 and 2020, and recent trade agreements are expected to expand access to several key markets.

Other Food Manufacturing enjoys the most growth of overall share of the industry’s GDP.

However, there are a number of challenges to industry competitiveness.

Over the past decade, the Canadian manufacturing industry has faced several challenges that have impacted its competitive position, such as fluctuation in the Canadian dollar, slow labour productivity, aging infrastructure and a significant increase in commodity prices.

An added difficulty for food and beverage processing businesses is that most of them are small and medium-sized businesses with fewer than 100 employees. Typically, research and development (R&D) is carried out by large firms with more than 500 employees. Considering that only 1 per cent of processing establishments in Canada have more than 500 employees, it is likely that a relatively small portion of the industry’s effort and workforce is dedicated to R&D activities.

Competition for scarce labour pools has also been a major challenge for the food and beverage processing sector and its global competitiveness. While the Canadian public

may be under the impression that the sector is home to many temporary foreign workers, the fact is that Canada’s competitors use much more foreign labour.

Despite these challenges, the food and beverage processing industry has continued to prosper in times of slow overall economic growth. For example, the industry’s GDP was

nearly 23% higher in 2016 compared to 2004. Conversely, the manufacturing industry in general has been unable to return to pre-recession levels (with GDP remaining 10% lower than its 2004 level).

In terms of proportion of GDP growth at the sub-sector level, analysis reveals that Other Food Manufacturing (including snack foods and coffee and tea) achieved the most growth at 13.0%, followed by Grain and Oilseed Milling (9.9%) and Fruit/Vegetable Manufacturing (6.8%). Sugar and Confectionery Product Manufacturing (-7.7%) was the only sub-sector to see its proportion of GDP decline, while Dairy Products and Baked Goods remained flat.

"Other Food Manufacturing including snack foods and coffee and tea achieved the most GDP growth at 13.0%, followed by Grain and Oilseed Milling at 9.9%."

In Budget 2017, the Government of Canada announced a new vision for Canada’s economy as a global leader. The Government created six economic strategy tables aimed at increasing the innovation of several sectors, including the agri-food sector. The report produced by the Agri-Food Table proposed action in the following five key areas to strengthen the Canadian agri-food sector.20

There are, and will continue to be, many opportunities for Canadian food and beverage processors to capture a significant share of expanding international markets. The global demand for food is expected to rise by 70 per cent between 2009 and 2050,21 fueled by a growing population and an expanding middle class that will consume considerably more protein than is the case today. Many of these middle-class consumers will want to know their food has been produced in a safe and environmentally sustainable way and are likely to favour agricultural products from countries such as Canada where environmental, labour and food safety and quality standards are considered to be world-leading.22

Canada’s processed food and beverage products are already exported to more than 190 countries, although the majority of these exports are concentrated in six major markets: the United States, China, Japan, Mexico, Russia and South Korea. The United States is Canada’s top export market, accounting for more than 70 per cent of total food and beverage exports, while Canada remains the largest export market for U.S. agricultural products.

Exports of Canadian processed food and beverage products increased by 22% between 2016 and 2020, while imports grew by about half that rate (13%). As a result, Canada moved from a trade deficit in processed food and beverage products in 2012-2015 to a trade surplus from 2016 onwards. The industry had an overall trade surplus of $4 billion in 2020.23

Recent international trade agreements, such as the Canada-European Union Comprehensive Trade Agreement (CETA)24, the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP)25 and the Canada-United States-Mexico Agreement (CUSMA)26 are increasing access for Canadian exporters in three of the largest trading regions in the world. This puts Canada in a strong position to capture a significant share of the growing global demand for food and beverage products.

Furthermore, as of the beginning of 2017, a customs tariff order repealed or amended approximately 200 different tariffs on imported food ingredients used in the agri-food processing industry, including certain fruits and vegetables, cereals and grains, spices, fats and oils, food preparations, and chocolate products. Reducing tariffs on manufacturing inputs helps lower production costs for Canadian businesses to enhance their overall competitiveness, both domestically and abroad.

"Breaking down barriers interprovincially will also further enable companies to reach international markets."

Both the Advisory Council and the Agri-Food Table clearly identified significant

opportunities for growth in Canada’s domestic market as well, with the Council noting

that Canada processes only half of its own agricultural output.27 The Agri-Food Table cited the rising share of imports in the growing Canadian processed food market – up from 22 per cent in 2007 to nearly 30 per cent in just 10 years – as a lost opportunity for Canada’s food processing sector28 and recommended a 27 per cent increase in the domestic sale of Canadian agricultural and food processing products by 2025, rising to $140 billion from $110 billion in 2017.29

Domestic market growth should be made easier by the Canadian Free Trade Agreement

(CFTA), which was put into place in the summer of 2017. It focused on eliminating barriers that restrict the movements of goods and services within Canada, providing the opportunity to capture a greater share of the domestic market. Breaking down barriers interprovincially will also further enable companies to reach international markets, by increasing their production domestically (i.e., attaining a critical mass of production volume for exporting to become financially viable).

To May 2020, and with few exceptions, the research suggests that the impacts of COVID-19 on the Canadian food and beverage processing industry have been very negative,30 to the point that close to half of surveyed companies (43%) were feeling under threat. The situation appears to be most dire in Quebec and relatively less severe in the Meat Product Processing sub-sector.

A startling 59% of surveyed businesses reported a decline in customer orders. In the face of such a shock and some abrupt shifts in consumer consumption habits, the industry has had to reconfigure workplaces to protect the health of employees, increase production in some areas and shift production in others.

More than seven-in-ten (71%) surveyed companies reported that they have taken at least some form of action in response to COVID-19. The most common responses were to reduce workers’ hours (43%) or conduct layoffs (41%). However, a comparison of similar data for Canadian businesses as a whole suggests that the food and beverage processing sector has been better able to weather the initial stage of the pandemic, than most other sectors of the economy.

Of companies feel under threat

Of companies have taken some form of action in response to COVID-19

Reduced workers' hours

Conducted layoffs

“59% of surveyed businesses reported a decline in customer orders. In the face of such a shock and some abrupt shifts in consumer consumption habits, the industry has had to reconfigure workplaces to protect the health of employees, increase production in some areas and shift production in others.”

The immediate economic and financial consequences of the COVID-19 global pandemic are starting to be understood. The medium and longer-term impacts of COVID-19 on Canadian businesses, however, cannot be estimated given the high levels of epidemiological and economic uncertainty that persists around the world. The Canadian food and beverage processing industry is a global industry with heavy reliance on both exports and imports. Until full implementation of an effective COVID-19 vaccine strategy is realized, deep uncertainty will remain. Even short-term predictions are challenging to make. To illustrate this, consider that in April and May 2020 more than one in four surveyed food and beverage food processors (26%) were unable to predict their production capacity for the upcoming month.

The results of a survey of Canadian food and beverage processors suggests that the initial impacts of COVID-19 on the sector have been very negative. The nature of these impacts, and of how companies have coped, are discussed following.

"Until full implementation of an effective COVID-19 vaccine strategy is realized, deep uncertainty will remain."

Various chains of events have impacted the industry resulting in improvised responses and adaptations. Immediate, large shifts in consumer demand for food and beverage products have focused on grocery retailers and away from restaurants and hospitality outlets. This has required rapid adjustments: sudden changes in packaging (e.g., wholesale to retail types of packaging in dairy), types of products in demand at the retail level (e.g., yeast, flour), and “panic buying” of certain food items. At the same time, significant declines in customer orders have occurred in many sub-sectors as the restaurant, tourism and hospitality industries have largely shut down. In response, the industry has had to reconfigure workplaces to protect the health of employees, increase production in some areas and shift production in others. It is also important to appreciate that the demands placed upon this industry are unique in many ways, particularly given that businesses are operating as an “essential service” to maintain the food supply chain for Canada and the world.

Following is an analysis of immediate and short-term impacts that COVID-19 is having on the industry. Because the pandemic can exert such deep and abrupt impacts from one day to the next, it is important to understand that the information and data we collected was during the period of April to June 2020, with the main source being a combined phone/online survey of 470 companies. Other sources included media reports, Statistics Canada data, and government and industry websites.

According to the survey, most employers in the sector have experienced a decline in customer orders (59%), while close to half (47%) reported a reduction in cash flow. Quebec had the largest number of companies report a decline in customer orders (70%), followed closely by Atlantic Canada (67%). In contrast, just 37% of companies in the Prairie provinces (Alberta, Saskatchewan, Manitoba) reported a similar decline. Consistent with production declines, more than 70% of companies across sugar and confectionery, seafood and beverage sub-sectors reported experiencing declines in customer orders. In addition, the beverage industry (41%) was twice as likely to report closures due to health

concerns. Declines in cash flows were also reported by a majority of beverage manufacturers and seafood processors.

The survey also found that 43% of businesses reported a decline in the number of workers available, thus exacerbating what had already been a tight labour market.

"Atlantic Canada experienced the most significant decline in the number of available workers."

Given that close to 6 in 10 surveyed companies have experienced a decline in orders, it is not surprising to see that fully half of respondents (51%) reported that production volumes had declined, with the average declined estimated to have been a staggering 49% since the outbreak of the COVID-19 global pandemic. In contrast, only 25% of companies increased their production volume, notably in meat processing where 46% reported a production increase compared to only 36% that noted a decrease.

Regionally, companies in the Prairies were more likely to report an increase in production volume, partially attributable to the strong presence of the meat processing industry, and a lower incidence of COVID-19 at the time compared to Ontario and Quebec.

The broadest question in the survey pertained to the general threat posed by COVID-19. The vast majority of companies (90%) perceive at least some level of threat from COVID-19, including significant proportions perceiving the threat to their businesses as “high” or “very high”.

Looking at a sub-sector analysis, nearly three-quarters of sugar and confectionery companies reported laying-off workers (73%), while 60% reported reducing workers’ hours. Companies in the animal food (15%), meat (25%), and grain and oilseed milling (26%) sub-sectors were the least likely to report lay-offs.

More than seven-in-ten (71%) surveyed companies reported that they have taken at least some form of action in response to COVID-19. The most common responses were to reduce workers’ hours (43%) or conduct layoffs (41%). Both of these actions, however, were taken somewhat less frequently than the average across all Canadian manufacturers (47% and 50% respectively) as reported in the Canadian Survey on Business Conditions. Similarly, a higher proportion of food and beverage processors reported not taking any action (29%) compared to 18% of Canadian manufacturers. Taken together, these results suggest that the industry has been better able to weather the initial stage of the pandemic than the broader manufacturing sector.

"Consumers are buying more groceries and eating at home."

Considerable levels of effort have been made in many sub-sectors to coordinate the rate of production of raw products (e.g., milk, seafood, vegetables) by farmers and harvesters. Employers were able to meet the slow down among various processors while adjustments to lines were made, products adapted, and productivity and plant closures addressed. For example, dairy processors worked with dairy farmers to lessen the volume of production of raw product. Farmers were able to reduce volumes by changing cows’ diets while increasing cows’ rest periods between calves.35, 35 Dairy manufacturers converted extra raw product into products with longer shelf-lives (e.g., cheese, butter, condensed milk) to avoid wastage, while also providing additional donations to foodbanks.36, 37

In seafood processing, Atlantic seasons opened later for lobster and crab and some daily quotas were placed on harvesters to accommodate the challenges being faced by seafood processors who had to react to changes in consumer demand and acute labour shortages. Potato farmers reduced crop sizes to accommodate the backlog of raw product that existed with producers who experienced large drops in demand for french fries caused by bar and restaurant shutdowns.38

It has been over a year since the COVID-19 global pandemic was declared. The situation has been difficult for all businesses with many layoffs and closures across the country. That said, the 2020 employment level for food and beverage processors was at 98% of the 2019 level. For comparison purposes, manufacturing without food and beverage processing was at 91% of its 2019 level and the Canadian economy as a whole at 92% of 2019 employment level. Food and beverage processing has outperformed manufacturing and the economy, in addition to this, wages have risen across the food sector (NAICS 311) by $2.65/hour from 2019.

Being designated as essential workers and providing stable employment in a turbulent time has helped the industry retain people, however there will be a new challenge on the horizon as the rest of the economy opens back up. Increased competition for workers from other sectors that were hit harder by the pandemic, is to be expected.

The industry will also need to continue to build on its successes and highlight the important role it plays in the economy and the lives of all Canadians.

"Food and beverage processing has outperformed manufacturing and the economy, in addition to this, wages have risen across the food sector by $2.65/hour from 2019."

Five key trends are expected to impact the future of food and

beverage processing in Canada:

COVID-19 is also expected to have a lasting impact on the sector. This issue is discussed in Section 3 – COVID-19 Impacts.

deficit in the available supply of water is expected by 2030

more undegraded arable land will be needed to meet crop demands

people by 2030. (The needs of a global consumer base is expected to surpass this).

“In the realm of consumer tastes, the dominant trends are heathy eating and drinking, and rapid growth in demand for specialty products.”

"Climate change can be viewed as a double-edged sword, replete with challenges but also providing significant opportunities."

The success of food and beverage processors is affected by many variables, including consumer preferences, Canadian and international regulatory regimes, trade agreements, changes in technology and climate change. Several major trends are expected to shape the future of manufacturing, and of food and beverage processing in particular:

Consumers in Canada, like those in many countries, are increasingly choosing food and beverage products that are healthier and produced in a more sustainable way, creating a demand for new and innovative products and the reformulation of existing ones. This includes an overall trend to add healthy fats in foods and reduced use of sugar and simple carbohydrates. There is also a move toward low-sodium foods and those that address

special dietary requirements, such as gluten-free, vegetarian and vegan products. Consumers are also interested in high-protein and alternative-protein products, new or uncommon flavours, and artisanal and organic products.

Younger Canadians, Generation Z and Millennials, are more likely than previous generations to choose their food based on dietary sensitivities and personal values, such as ethically sourced food products, vegetarian and vegan preferences, and sustainable production methods. They are also more likely to substitute plantbased alternatives for meat and meat products, and to consume

products that are organic, contain “clean” ingredients, are glutenfree, dairy-free and locally grown. These shifts are having a significant impact on the food and beverage processing industry, in particular, grain and oilseed milling, and dairy and meat sub-sectors.

"Other consumer trends affecting Canadian food and beverage processors include the growing demand for convenience foods, meal kits and quick, ready-to-cook options, as well as smaller portions and package sizes that meet the needs of smaller families and individuals."

Changing demographics have boosted demand for specialty products, including Halal items and other foods and beverages that cater to an increasingly diverse ethnic population. Ethnic food markets, which generated an estimated $49 billion in spending in 2015, have been projected to increase to $97 billion in 2020. The Canadian food and beverage processing industry must adapt to this changing dynamic, not only to capture more of the domestic market but also to increase its share of global opportunities.

Other consumer trends affecting Canadian food and beverage processors include the growing demand for convenience foods, meal kits and quick, ready-to-cook options, as well as smaller portions and package sizes that meet the needs of smaller families and individuals.

Taken together, these consumer trends suggest that the sector will need to become more diversified and specialized. Whereas before, a company might have produced three or four products to meet a fairly homogenized consumer market, today and tomorrow, a significantly expanded line of products may be required. The Canadian alcoholic beverage market is a good example of this.40

Several regulatory bodies oversee and enforce food and beverage production and safety in Canada at the federal level, including the Canadian Food Inspection Agency, Health Canada and Measurement Canada. There are also several agencies, laws and regulations relevant to the food and beverage processing industry in each of the provinces and territories.

In January 2019, an updated regulatory framework took effect in Canada under the Safe Food for Canadians Act and the Safe Food for Canadians Regulations. The new framework combined 14 previous regulations into a single framework to reduce inconsistencies and administrative costs and increase innovation opportunities for business.

Additional regulatory measures, including Canada’s Healthy Eating Strategy,41 are giving consumers even more ways to make informed decisions about the foods and beverages they purchase. As part of the Strategy, food labelling regulations were updated in 2016 revising the requirements for nutrition facts tables and lists of ingredients to make it easier for consumers to compare similar products and make healthier choices. The federal government has also proposed introducing mandatory front-of-package labelling for foods that are high in saturated fat and/or sugars and/or sodium.

While this is likely good news for consumers, these changes present challenges to processors. Added costs incurred to comply with new measures limit the funds available to invest in new product development that will meet changing consumer preferences.

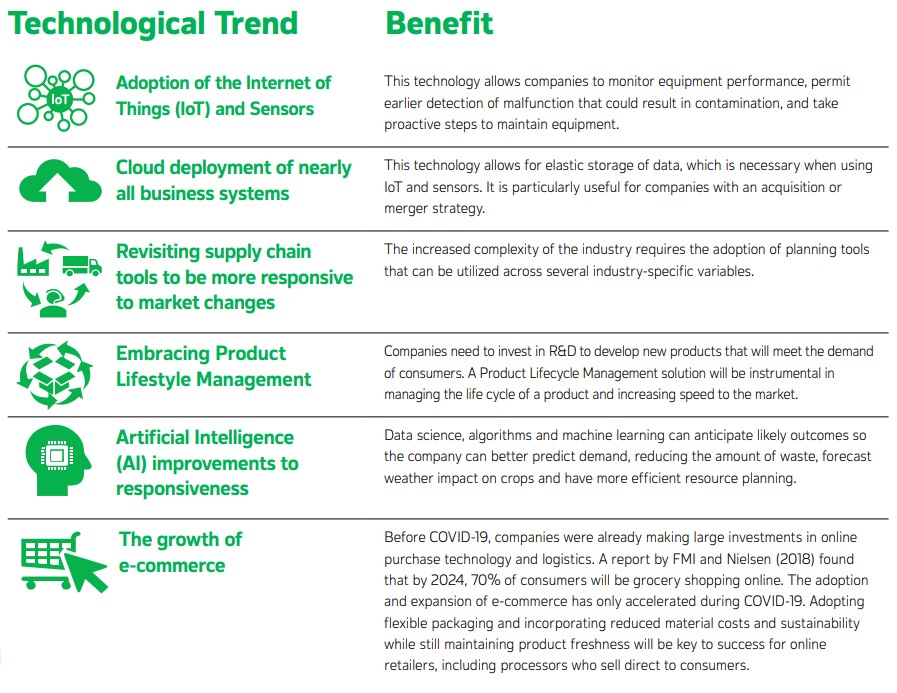

Innovation is a key component in keeping operations running smoothly and efficiently in the food and beverage processing industry. Several emerging technologies are increasing the productivity and quality of food and beverage processors. See the following six examples of technological trends expected to impact the industry in the coming years:

All the trends described above are part of what some have dubbed “the fourth industrial

revolution”, known commonly as Industry 4.0.

Industry 4.0 is the next stage in the evolution of production systems. Its impact will be felt across all sectors of Canada’s economy. In food and beverage processing, Industry 4.0 will lead to the creation of “smart factories”, which differ from traditional factories in two ways. First, smart factories will enable machines, devices, sensors, and workers to connect to and communicate with each other. Second, smart factories will link real world environments with precise digital counterparts to create cyber-physical systems.

Industry 4.0 will allow for an integrated supply chain that will enable businesses to anticipate and respond to consumer needs, reduce the time required for research and development, and optimize the use of labour. It will also provide health and safety benefits for consumers by increasing the traceability of ingredients and improving the speed and effectiveness of product recalls.

In June 2019, RBC and Microsoft announced the launch of a new digital program aimed at optimizing food manufacturing operations through Industry 4.0 principles.

As with the last industrial revolution, the expectation from a labour market standpoint is that 1) fewer workers will be required (thus easing the pain of labour shortages), and 2) require workers to have a higher level of skill and education.

"Industry 4.0 will allow for an integrated supply chain that will enable businesses to anticipate and respond to consumer needs, reduce the time required for research and development, and optimize the use of labour"

Recreational use of cannabis was legalized in Canada on October 17, 2018. Initially limited to dried or fresh cannabis and cannabis oil, legalization was extended in October 2019 to permit the recreational use of cannabis edibles and infused beverages and alternative cannabis products. This change is creating new opportunities for food and beverage processors but also adds a new dimension to the operations of companies who pursue

such opportunities, including a new level of regulatory oversight to minimize the public health and safety risk posed by such products and preventing accidental consumption by youth.

The final regulations ban the production of all cannabis products in the same building as food products. In terms of packaging and labelling, the current regulations for dried cannabis are being applied to cannabis edibles and infused beverages, extracts, and topicals. In addition, the regulations are being amended to make it easier for additional product information to be displayed (e.g., list of all ingredients, indication of any allergens, “best before” date, a cannabis specific nutrition fact table). This is all labelling information that the food and beverage processing industry is familiar with, providing it with a competitive edge over established dried cannabis flower producers.

According to the Brookfield Institute, the demand for cannabis in Canada is expected to exponentially increase, driven by the sale of edibles and innovative new products.42 More specifically, Brookfield predicts that the cannabis economy will create immense new market opportunities in retail, product development, and healthcare, and that individuals soon may spend their entire professional career working in the cannabis industry and target their skills

training to meet the demands for innovation in the sector.

The recent survey of food and beverage processors asked about processors moving into infused beverages or edibles. The responses were clear that it wasn’t an area where many food and beverage processors were looking to expand with 79% saying no, only 4% saying yes and 18 % unsure or would consider it at a later date.

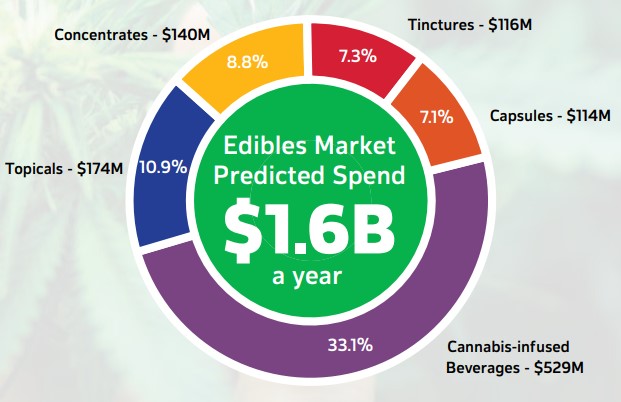

According to Deloitte’s latest annual report on Canada’s cannabis industry, it projects that the edibles market is worth at least $1.6 billion a year. For its part, Health Canada estimates cannabis products, other than dried cannabis, will account for just under half of the total market, a similar amount to the portion of sales found in other jurisdictions with legalized cannabis such as California, Colorado, and Oregon. In all, cannabis edibles and infused beverages are believed to generate higher profits for retailers than cannabis products that are already legal. Deloitte predicts Canadians will spend annually $529 million on cannabis-infused beverages, $174 million on topicals, $140 million on concentrates, $116 million on tinctures and $114 million on capsules.43

Growth in the cannabis industry, and edibles specifically, is already translating into increased demand for labour. According to Indeed.com, job openings in the cannabis industry tripled from July 2018 to July 2019 and were expected to keep growing as edibles became legal.

More information on the cannabis sub-sector can be found in FPSC’s 2020 labour market report, Cannabis Industry and Edibles.44

The food and beverage processing industry will increasingly face constraints on its production because of natural resource limitations induced by climate change. The industry is especially vulnerable to the effects of climate change because many early stages in the food and beverage supply chain depend on weather conditions and other environmental factors.

Consider the following tensions:

These issues, along with the larger impact of climate change on labour productivity, transportation, and energy, will combine to constrain the supply of food and beverage products available for processing.

However, climate change can also present opportunities for some processors, for example, through improved growing conditions for Canadian grapes used by Canadian winemakers.45

There are a number of opportunities – reducing carbon footprint, enviro-friendly packaging, use of ethical/green supply chains – that exist for businesses to distinguish themselves in the eyes of their employees and customers.

This section covers a significant amount of ground. We begin by noting that the food and beverage processing sector experienced very strong employment growth in 2017, 2018, and 2019 after almost a decade of stagnation, with the largest employment gains in the Beverage Manufacturing sub-sector. Despite the pandemic, 2020 employment was 98% of 2019 and still above the 2018 level. This section also includes a discussion on the sector’s relatively…. of the sector’s relatively high job vacancy rate and the financial impact that unfilled positions are having. Essentially, a high volume of vacancies restrict output, leading to lost revenues for businesses.

Persistent job vacancies, along with other labour market challenges (e.g., public perceptions of work in the food and beverage processing sector), have obvious implications for the sector’s ability to reach some of the ambitious targets set for it by the Agri-Food Table (e.g., $85 billion in export sales by 2025). Some of these challenges are highlighted below.

Turning to the future, this section highlights forecasted hiring needs based on two different growth scenarios and ends with a presentation of workforce demographic and occupational profiles, including an analysis of compensation and unionization.

Skilled trades workers account for the total industry’s workforce.

Industry 4.0 could reduce industry hiring needs by

workers needed to maintain status quo in 2025.

“The industry had a very strong employment growth in 2017 and 2018 after almost a decade of stagnation.”

The industry had very strong employment growth in 2017 and 2018 after almost a decade of stagnation. Notwithstanding, the employment vacancy rate in 2018 was about 25% higher than it was for manufacturing in general (3.8% vacancy vs 3.0%).

The analysis presented in this report highlights the actual cost of job vacancies in the industry, and it’s sobering. Estimates show that a single unfilled position in the food and beverage processing industry could cost businesses as much as $190 per day in lost net revenue46. Aggregated over the entire sector, losses from job vacancies could total up to an estimated $8.5M in net revenue per day.

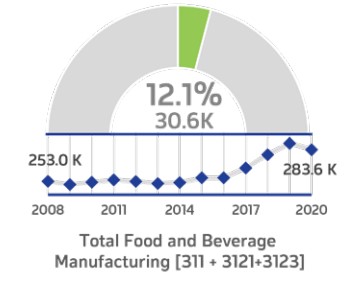

The number of people working in the industry increased by just over 10 per cent between 2010 and 2020, from just over 250,000 to just over 280,000, with most of this growth occurring in 2017, 2018, and 2019.47 The industry remains the biggest provider of manufacturing jobs, accounting for 19.5 per cent of total manufacturing employment in 2020, an increase from 201948 and up from just over 13 per cent in 2001.49

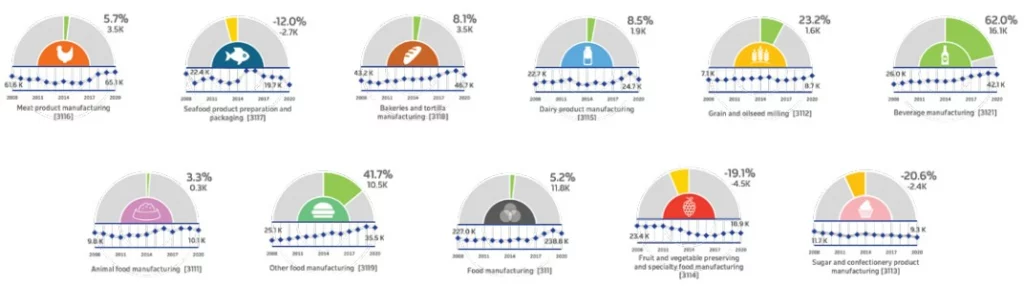

There are significant differences at the sub-sector level, with the largest employment gains in the last decade in the Beverage Manufacturing sub-sector (+42%), followed by Other Food Manufacturing (+30%) and Grain and Oilseed Milling (+18%). Some other sub-sectors saw employment declines between 2011 and 2020, including Fruit and Vegetable Preserving and Specialty Food Manufacturing (-19%), Sugar and Confectionery Product Manufacturing (-9%) and Seafood Product Preparation and Packaging (-8%).50

Yet despite this growth, the job vacancy rate in 2019 (3.8 per cent 51 ) was the highest annual rate since Statistics Canada’s Job Vacancy and Wage Survey began in 2015 and above the 2.9 per cent job vacancy rate for the overall manufacturing sector. There were also significant regional differences in the food and beverage processing industry, with the highest vacancy rates in PEI (8.6%) and the lowest in Manitoba (1.6%).

Looking ahead, the Agri-Food Table set an ambitious target for agri-food and seafood export growth in its 2018 report, aiming for $85 billion in export sales by 2025, a 32% increase from $65 billion in 2017 . The report also set a target of $140 billion in domestic

sales by the same year.

So, what is needed to actually achieve these targets? There is no doubt that a significant influx of new workers is needed, but how many? Consider the following two scenarios – one that models the number of workers needed to simply keep going at the status quo (the “baseline scenario”), the other a model of how many workers are needed to meet the growth target (“the growth scenario”):

As with any economic modeling a number of assumptions were required, first both scenarios assume labour replacement demand due to retirements which amounts to 2.0% of the total workforce annually. Second, an assumption of 1.0% growth in labour productivity to capture the impact of workers and their equipment becoming more effective over time. In both “scenarios” growth in imports and domestic consumption is tied to forecasts of Canadian population growth, while growth in inter-industry salesis based on a forecast of Canadian real GDP growth.

Also, forecasts of hiring needs must consider two different types of labour demand:

Replacement demand represents the primary source of demand for new workers in both scenarios due to the aging workforce seen both in the manufacturing sector as a whole and the food and beverage processing industry specifically.

When both expansion and replacement demand are considered together, the total hiring requirement for the industry over the 2020-2025 period in “the baseline scenario” is estimated at about 32,000, or 11% of the industry’s workforce in 2020. Put another way, the sector will need about 32,000 new workers just to maintain the status quo over this this period.

"A high volume of unfilled positions can restrict output, leading to lost revenues for businesses and the industry"

In “the growth scenario”, the total hiring requirement rises to 56,000 workers, equivalent to 20% of the industry’s 2020 workforce.

These figures could be even higher if, for example, labour productivity rates are below anticipated levels as some experts predict. Clearly, recruiting and retaining qualified workers will be crucial to ensuring the continued growth of the industry, as well as adopting new and innovative ways of processing.

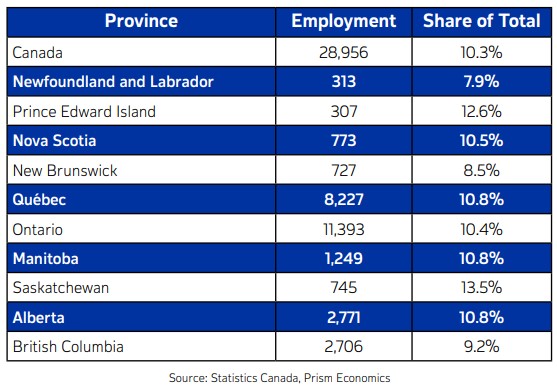

Canada’s food and beverage processing sector (NAICS 311) employed an estimated

29,000 skilled trades workers in 2019, accounted for 10.3% of the total workforce.

Skilled trades made up the largest proportion of the food manufacturing workforce in the

provinces of Saskatchewan (13.5%) and PEI (12.6%), while Newfoundland and Labrador

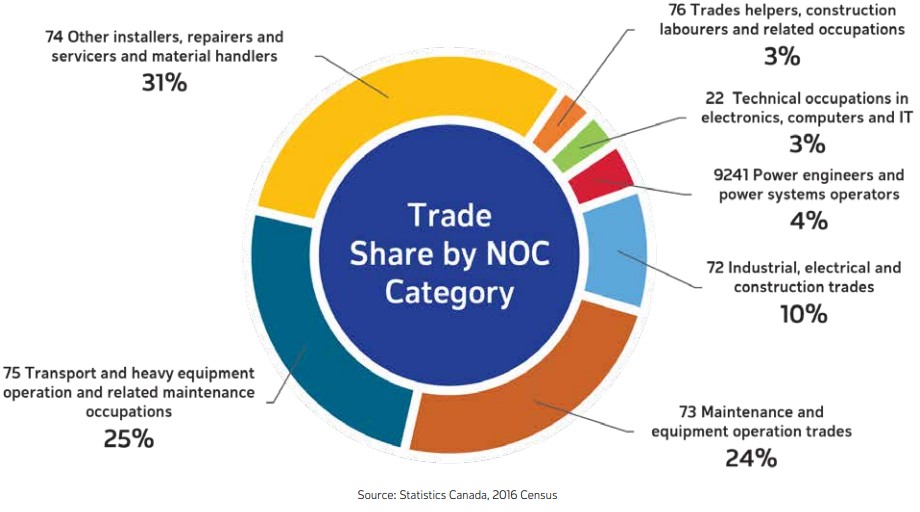

had the lowest share (7.9%). Trades working as Installers, Repairers and Service

Material Handlers (NOC 74) account for 31% of trades, followed by Transport and heavy

equipment operation and related maintenance occupations (25%) and Maintenance

and equipment operation trades (24%). The industry also employs significant numbers

of industrial, electrical and construction trades, Power engineers and power systems

operators and Technical occupations in electronics, computers and IT (see Figure 1).

Looking across individual food manufacturing sectors, Beverage manufacturers employ

the largest share of skilled trades (20.6%) followed, flowed by Grain and oil seed

milling (19.1%) and Animal food manufacturing (17.3%). Seafood processors (7.2%) and

Bakeries (7.4%) employ the fewest (see Figure 3).

Skilled Trades Employment in Food Manufacturing, by Province, 2019

Skilled Trades Employment in Food Manufacturing, by Province, 2019

Skilled Trades Employment Share of Total Food Manufacturing, by Trade Group

Skilled Trades Employment in Food Manufacturing, by Food Manufacturing Sector

There are several potential barriers to achieving the Agri-Food Table’s targets for the industry, including a lack of investment, trade barriers and tight labour markets (restricted foreign workers). To meet these targets, all levels of government must work alongside

the industry to improve competitiveness and investment. There must also be development of a skilled labour pool and changes to regulatory barriers hindering growth.

One way to mitigate these barriers is investing in new technologies, particularly integrating Industry 4.0 production processes. Research shows that Industry 4.0 integration could boost labour productivity by as much as 0.8% annually.

That may not sound like much, but this research shows that complete Industry 4.0 integration of the food and beverage processing industry over the next five years could reduce estimated hiring requirements by as much as 20%, from 56,000 to just over 43,000. While it is unlikely the entire industry will be able to move fully to Industry 4.0 in the near term, it’s encouraging to learn many businesses have already begun this process. In the 2020 employer survey, three-in-four (78%) companies reported that their organization has made at least some effort towards complete integration of Industry 4.0 production processes, consisting of investment into automation, digitization or wireless interconnectivity. One-in-four (23%) surveyed companies had already achieved a high level of Industry 4.0 integration. As organizations continue to adopt more advanced technology, additional training will be required to ensure employees are adequately equipped to use such technology.

"Research shows that Industry 4.0 integration could boost labour productivity by as much as 0.8% annually."

Public perceptions of working in the sector has a significant impact on the labour market. To understand this better, FPSC conducted a survey in 2018 to gather insights into the perceptions, interests and motivations of key target audiences: youth, Indigenous People, New Canadians and those with a tenuous connection to the workforce (currently unemployed and/or frequently unemployed). Members of the general public were also

surveyed to provide a benchmark.

In total, 2,089 people responded, 972 of which were part of the youth group, 506 part of the Indigenous People group, 500 part of the new Canadians group, and 1,205 part of the unemployed group. Due to the nature of these groups, there was some overlap between them. In other words, some people were included in more than one segment. The general public benchmark sample included 1,248 people.

Similar to the general public, the four target audiences had a relatively low awareness

of the food and beverage processing sector, but broadly viewed the sector more

positively, and were more willing to consider taking a job in the sector. Specifically, the

survey asked respondents to evaluate four specific jobs in the sector, from an entry

level position to operations manager. The target audiences were much more interested

than the general public in applying for all four jobs profiled. An Operations Manager

position generated the most interest – 37% new Canadians, 32% of youth, and 28% of

Indigenous People said they would apply, compared to only 18% of the general public.

The target audiences, however, were also more likely to associate the sector with

negative terms. For instance, they were less likely than the general public to use terms

“happy workforce”, “innovative”, “high pay” and “high skill” in reference to jobs, and more

likely to use terms like “slow” and “not able to progress.”

"As Generation Z ages into Younger Millennials, advancement becomes more important. They hope to see a path forward and are particularly keen to learn new things."

The hypothesis that certain labour market segments (i.e., Youth, Recent Immigrants, Indigenous People and those who are tenuously attached to the labour force) are more predisposed and open to working in the food and beverage processing industry

than other Canadians was confirmed.

Consistent with the results of the initial analysis described above, recent immigrants emerged as a particularly promising segment. The deep dive analysis, however, also highlighted Indigenous People as equally receptive to working in the food and beverage processing industry, if not more so.

Analysis of Statistics Canada labour force data suggestes that the window of opportunity for hiring recent immigrants narrows over time. In 2018, the unemployment rate among immigrants who had lived in Canada between five and 10 years was about one-third lower than it was for those who had live here for no more than five years.

The most striking aspect of the industry’s workforce is the age demographic.

24% of the workforce is aged between 55 and 64, with the majority of these individuals

eligible to retire in the next 10 years. Men make up 60% of the workforce and immigrants

31% – an overrepresentation when compared to only 23% of the overall labour force.

Indigenous Peoples make up 3% of the workforce which is 1% less than the overall

labour force.

More than half of the industry’s workforce is made up of labourers followed by process control and machine operators, and fish plant workers. The average hourly pay continues to lag behind other manufacturing sectors, but the gap has narrowed significantly over the last 10 years.

Unionization within the industry remains at a higher level relative to other sectors of the Canadian economy, with 27% of food and beverage processing workers unionized in 2018. Close to 60% of unionized workers are in Ontario.

Employing the largest proportion of visible minorities is Meat Manufacturing

Men make up

of the food and beverage manufacturing workforce

of immigrant workers come from the Philippines

“The defining demographic characteristic of the sector’s labour force is an overrepresentation of immigrants. Approximately one-third (31%) of the industry’s workforce consists of immigrants, compared to only 23% of the overall labour force.”

Perhaps the defining demographic characteristic of the sector’s labour force is an overrepresentation of immigrants. Approximately one-third (31%) of the industry’s workforce consists of immigrants, compared to only 23% of the overall labour force.

Men make up 60 per cent of the workforce, with the largest share of male workers in the Grain and Oilseed Milling sub-sector (74%), followed by Beverage Manufacturing (72%), Animal Food Manufacturing (68%) and Dairy Product Manufacturing (67%). Just two sub-sectors have a higher proportion of women than men working in them: Bakeries and Tortilla Manufacturing (52%) and Sugar and Confectionery Product Manufacturing (51%).

Overall, there is a higher proportion of men than women working in management positions and as tradespeople or transport and equipment operators, while women make up a larger share of business, finance and administration positions, and sales and service occupations.

The majority of the industry’s workforce is between the ages of 25 and 54, although this cohort has declined in size by more than 10 per cent since 2006. One-quarter (24%) of the workforce is aged between 55 and 64, with many of these workers eligible to retire over the next decade.

Approximately one-third (31%) of the industry’s workforce consists of immigrants, compared to only 23% of the overall labour force.

Further analysis reveals that in 2016 most of the immigrants who worked in food and beverage processing arrived in Canada between 1991 and 2010, while more recent immigrants (those who arrived in Canada between 2011 and 2016) made up five per cent of the workforce. The latest survey showed that recent immigrants (2014-2019) increased to 9%. In the census, 31% of the workforce were identified as immigrants (all lengths of time in Canada). Given, the recent survey that indicates 9% of immigrants had arrived in the last 5 years, we can conclude that employers are doing well in retaining immigrant workers.

The survey also showed that the most common nations that the industry’s immigrant workforce come from are Philippines (36% of respondents have staff from there), India (33%), China (27%), Mexico (24%) and USA (20%). There were 10 nations that appeared in the responses of at least 10% of employers. The survey also looked at which language groups are spoken by staff, Canada’s official languages were clearly top followed by Southern European Languages (e.g, Spanish, Portuguese and Italian), South East Asian languages (e.g., Thai, Vietnamese and Tagalog) and South Asian (e.g., Punjabi, Hindi and Urdu).

The highest proportion of immigrants work in Meat Product Manufacturing (43%), Bakeries and Tortilla Manufacturing (43%) and Other Food Manufacturing (42%). The sub-sectors with the lowest proportion of immigrant workers are Seafood Product Preparation and Packaging (9%) and Animal Food Manufacturing (15%).

"The recent survey concludes that employers are doing well in retaining immigrant workers."

Indigenous People make up about three per cent of the industry’s overall workforce, spread across all sub-sectors, except Seafood Product Preparation and Packaging, where they make up 11 per cent of employees. On a provincial level, the highest proportions of Indigenous workers in the industry are in Nova Scotia (10%), Newfoundland and Labrador (9%) and Saskatchewan (9%).

Visible minorities53 account for just over one-quarter (28%) of the food and beverage processing workforce, slightly higher than the proportion working in the overall manufacturing sector (23%). The sub-sector employing the largest proportion of visible minorities is Meat Product Manufacturing (41%) while Seafood Product Preparation and Packaging employs the smallest proportion (10%). This reflects in large part the demographics of the regions where these sub-sectors concentrate their activities.

More than half (55%) of the industry’s workforce has either a high school diploma or no certificate, diploma or degree of any kind, compared with 45% of the overall manufacturing workforce. Seafood Product Preparation and Packaging has the highest proportion of lower-skilled workers (72%), followed by Meat Product Manufacturing (61%) while Beverage Manufacturing has the lowest proportion (42%).

More than half of the industry’s workforce continues to be made-up of

labourers.

Average hourly wages in the sector still lag behind the average for the

manufacturing sector, but the gap has narrowed significantly over the past

decade.

While the rate of unionization in the sector had eroded over the past 10 years,

it remains somewhat higher than the average rate of union membership

across all sectors of the economy. Most of the union members in the sector

work for one of Canada’s five largest food and beverage processing industry

employers.

Find following an examination of the nature of jobs in the industry, as well

as their relative prevalence. We also present the results of a comparative analysis of wages and the extent of unionization today and over time.

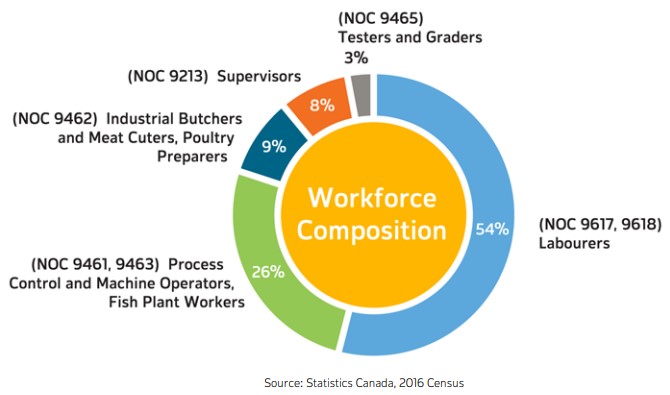

Labourers continue to be the largest category of workers in the food and beverage processing industry, representing 54 per cent of the workforce, followed by process control and machine operators and fish plant workers (26%) and industrial butchers and meat cutters, poultry preparers and related workers (9%). Supervisors account for eight per cent of the industry’s workforce, with testers and graders (3%) making up the rest.54

Men account for most workers employed as supervisors (68%), process control and machine operators (69%), and industrial butchers and meat cutters (69%). In contrast, women are more likely to be employed as testers and graders (61%), and fish and seafood plant workers (61%). Men and women are equally likely to be employed as labourers.

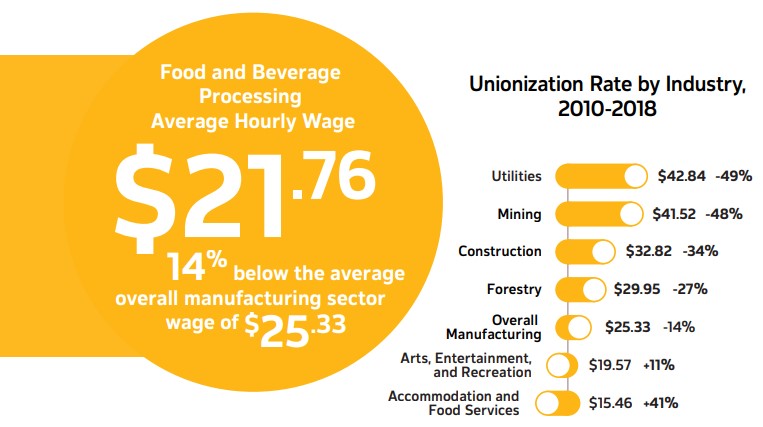

Wages in the sector are going up, but are still below the overall manufacturing sector. Average hourly wages in the sector in 2018 were $21.76 per hour55 for employees paid by the hour, compared with $18.14 per hour in 2008.56 This rate is about 14 per cent below the average of $25.33 for the overall manufacturing sector in 2018, though the gap has narrowed somewhat from the nearly 20 per cent differential between 2008 and 2018. Average hourly wages for food manufacturers are highest in Ontario and Alberta, most likely due to competition for labour from other industries, including other manufacturing sectors.57

The industry’s average hourly wage was also generally lower than that of similarly labour-intensive sectors. Sectors with higher wages in 2018 include forestry and

($29.95); construction ($32.82); mining, quarrying, and oil and gas extraction ($41.52); and utilities ($42.84). Lower wages may negatively impact recruitment efforts by food and beverage processors as they compete against these sectors for workers. Sectors with lower wages include arts, entertainment and recreation ($19.57), and accommodation and food services ($15.46).

For salaried employees in the industry, the equivalent hourly wages in 2018 was $32.47, about 12 per cent lower than equivalent hourly wages of $37.04 for

salaried workers in the overall manufacturing sector and $36.69 across all industries.

Unionization within the industry remains at a higher level relative to other sectors of the Canadian economy, with 27 per cent of food and beverage processing workers unionized in 2018. While this percentage has declined from the 32 per cent unionization rate seen during the period of 2010-2013, it is still above the average unionization rate of 24-25 per cent across all industries during the period 2010-2018.

Close to 60 per cent of unionized workers in the food and beverage processing industry are in Ontario, and approximately one-third of unionized workers in Canada are employed by one of the five largest employers in the industry (Black Diamond CheeseTM, Coca ColaTM, NestleTM, PepsiCo FoodsTM and SaputoTM).

When we examined unionization at a sub-sector level the research reveals that unionization is highest in the Meat Product Manufacturing subsector (51%), followed by Grain and Oilseed Milling (40%) and Dairy Product Manufacturing (35%). Three sub-sectors – Beverage Manufacturing (30%), Sugar and Confectionery Products Manufacturing (26%), and Fruit and Vegetable Preserving and Specialty Food Manufacturing (26%) – have unionization rates close to the overall industry average, while the four remaining sub-sectors – Animal Food Manufacturing (11%), Bakeries and Tortilla Manufacturing (17%),

Seafood Product Preparation and Packaging (18%), and

Other Food Manufacturing (21%) – have below average rates of unionization.58

This section draws heavily on survey data, including a 2020 survey of 740 facilities across the food and beverage processing industry. The survey had excellent coverage reaching processors in every province and at least 50 processors from every sub-sector, excluding cannabis product manufacturing. There was also representation from a variety of employer sizes, with just over half (56%) of the respondents selling products out of province and a third (35%) exporting to the USA.

companies in the industry reported that they have neither an HR department nor dedicated HR staff.

of employers face recruitment and retention challenges.

“The biggest challenge for employers is accessing a pool of qualified candidates, while skills training was identified as the second largest challenge.”

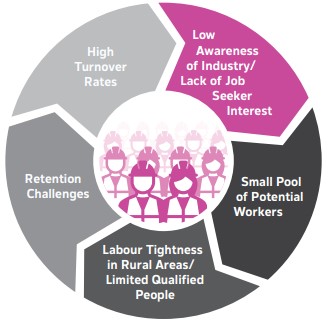

The top business challenge in the industry is a people challenge. Consider the following cycle: Low awareness and willingness to work in the industry leads to small pools of potential workers. This situation is compounded by labour tightness in the non-urban geographic locations of many businesses. Then, among the worker pools, skills are lacking which creates few qualified people that once hired, may lead to retention challenges and high turnover rates.

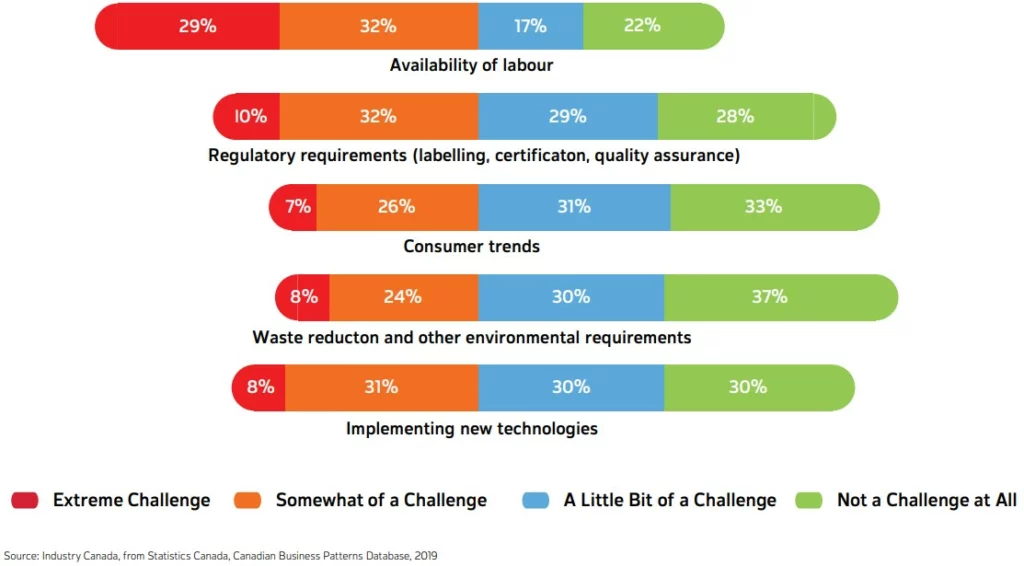

The research found that labour availability (e.g., lack of qualified applicants) is the top overall business challenge – ahead of coping with regulations. Implementing technology and meeting customer preference round out the top four priorities for employers. In addition to labour shortages, close to half of companies face turnover and retention challenges. According to a 2018 labour market survey, one of the factors making it more difficult for the food and beverage processing sector to find new workers, is a relatively low awareness of the industry among the general public. Raising awareness has proven to be a significant challenge. The 2020 survey found that employers were split on the best way to promote the sector to the public. That said, the previous 2018 survey also showed that once people learned about the industry, they were more receptive to working in it.

This section includes a discussion of strategies that employers have used to cope with labour shortages and retention challenges. For example, most say they have made a “concerted” effort to target young people and women. Online postings (e.g., LinkedIn) is the most used recruitment method; the survey also found that 16% of employers use the Temporary Foreign Worker Program. Crucially, this section also discusses approaches to skills development from both the employer and worker perspectives.

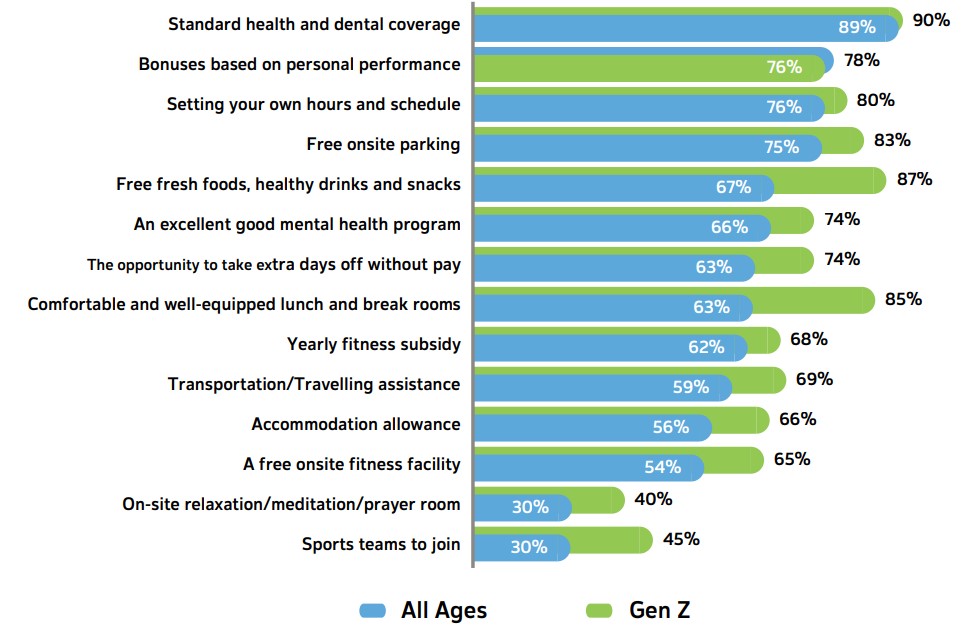

As discussed earlier in this report, FPSC’s 2018 labour force survey suggests that recent immigrants and Indigenous Peoples, and to a lesser extent youth and those with a historically tenuous attachment to the labour force, represent promising recruitment targets for the industry. Related to this, FPSC’s 2020 survey of labour participants found that health and wellness options (e.g., free fresh foods, healthy drinks and snacks, comfortable and wellequipped lunch and break rooms, and onsite fitness facilities) are very attractive to young people and women.

Prior to COVID-19, ongoing labour shortages in parts of Canada were expected to cause the food and beverage processing industry to continue its struggle to find workers.59

A 2018 in-depth sub-sector labour market analysis for the Seafood Product Preparation and Packaging conducted by FPSC found that, for example, acute labour shortages would worsen if nothing was done to change the situation.60 Specifically, the report estimated the number of unfilled vacancies at 1,800 in 2017 and projected that an additional 7,500 workers would be needed by 2030, simply to keep up with the attrition of retirement.61

FPSC released another detailed labour market information study in 2018, this one examined Canada’s Meat Product Manufacturing sub-sector, where there are roughly 1,600 businesses employing approximately 58,000 people (in 201762). This research found that more than half of businesses in the sub-sector were experiencing “chronic recruitment challenges”, leaving an estimated 7,300 positions unfilled in 2016. High annual turnover rates (in excess of 40 per cent) compounded difficulties for a sub-sector that was projected to need to hire approximately 32,000 additional workers by 2030 to replace retirees and fulfill growth expectations.63

Labour availability is the top overall business challenge, ahead of coping with regulations, implementing technology and meeting customer preference.

Of the 68% of employers who face recruitment and retention challenges, most describe the problem as persistent/on-going. The challenges of recruitment and retention are most keenly felt by Quebec companies. The evidence also suggests that recruitment and retention problems have worsened over the past year.

"The study finds that most Canadians (67%) want to stay with the same employer for as long as they can."

It is important to note that 4 in 10 companies in the industry reported that they have neither an HR department nor dedicated HR staff. The exception is Meat Product Manufacturing, where 73% have an HR department, by far the highest among the 11 sub-sectors.

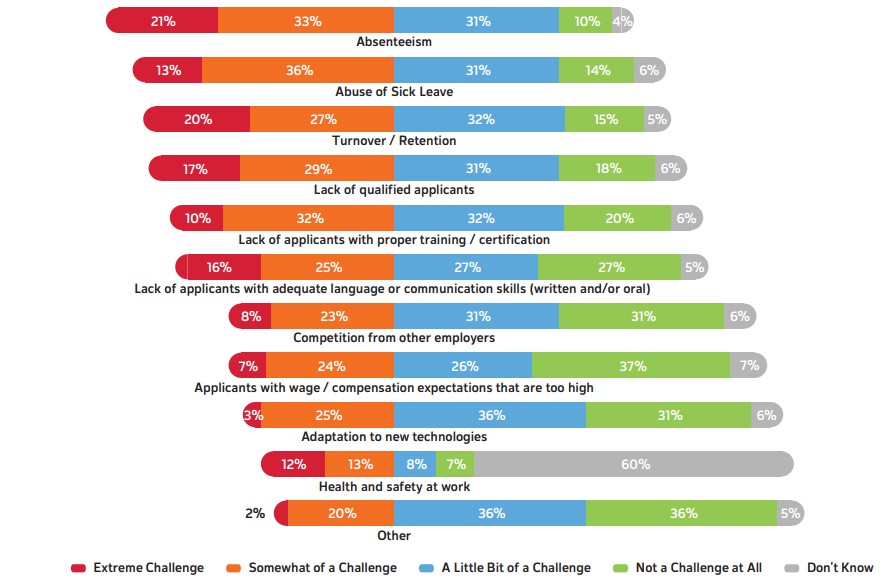

Employers were asked to assess the level of difficulty they experience with a range of specific HR issues, including those associated with hiring and retaining people.

The biggest challenge for employers is accessing a pool of qualified candidates. This was identified as at least somewhat of a challenge by 54% of survey respondents, including 21% who identified it as an extreme challenge. In Quebec, seven-in-ten (71%) employers reported this as at least somewhat of a challenge, compared to approximately one-third in Saskatchewan and Manitoba. Within the industry, the Dairy (70%) and Animal Food (67%) sub-sectors find this challenge more daunting, while employers in Beverage Manufacturing (37%) and Sugar and Confectionery (40%) considered it less of an issue.

Skills training was identified as the second largest challenge, with almost half of employers saying that a lack of applicants with proper training and/or certification is at least somewhat of a challenge (47%).

High wage expectations, turnover and retention, and absenteeism are all viewed as at least somewhat of a challenge by over 40% of respondents. Health and safety, which was identified as the most important HR issue in a 2011 industry survey, appears to be less of a concern in 2020.

The research also looked into the extent to which recruitment challenges were constant throughout the year, or intermittent/ seasonal. Only 32% of employers said that they have “no significant challenges”. Of the close to 7 in 10 who do face recruitment and retention challenges (68%), most describe the problem as persistent and on-going.

The prevalence of recruitment and retention challenges appears to vary depending on the region and sub-sector. For example, employers in the sector who operate in Alberta are much more likely to report experiencing no challenges in recruiting (46%) compared to those across the rest of Canada (26%). Conversely, companies in Quebec were twice as likely to report experiencing immediate or persistent challenges. Companies in the Dairy, Meat, Seafood and Bakery sub-sectors were more likely to report immediate and persistent challenges in the recruitment and retention of workers.

Most employers surveyed (57%) in 2020, said that the extent of their recruitment challenges had not changed over the previous year. More significantly, however, those who did report a change overwhelmingly indicated an increase (35%), as opposed to decrease (5%). Consistent with other results, it is clear that the situation is more dire in Quebec, where one half of companies (49%) reported growing recruitment challenges.

And of particular note, the research reveals that recruitment and retention tends to be more challenging in rural parts of Canada.

In 2020, FPSC released a study titled “Working Together – A Study of Generational Perspectives in Canada’s Labour Force”. This study examined generational perspectives about career related aspirations, expectations and preferences (e.g., learning, compensation) across the five generations that coexist in the workplace today.64 The study finds that most Canadians (67%) want to stay with the same employer for as long as they can. It is interesting to note that views on this question are fairly uniform across the five generations represented in the workplace.

"The Dairy, Meat, Seafood and Bakery sub-sectors were more likely to report immediate and persistent challenges in recruitment and retention."

Canadians said they are familiar with the food and beverage processing industry.

of respondents did not know how much they spend on training annually.

of employers offering employee benefits reported providing extended health and drug plans.

“Recent immigrants and Indigenous Peoples, and to a lesser extent youth represent promising recruitment targets for the sector.”

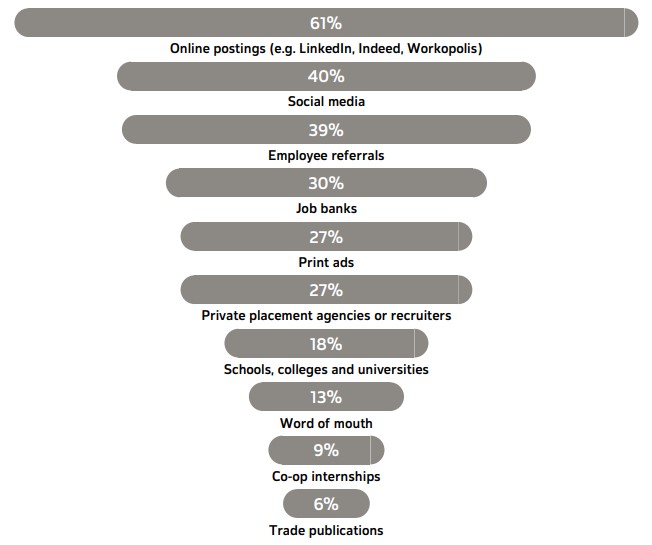

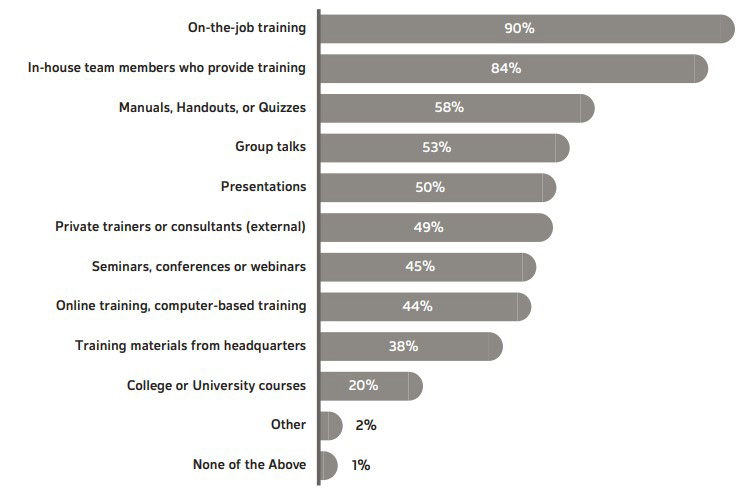

It will come as no surprise that nearly all employers (92%) surveyed allocate at least some resources towards recruiting employees. These employers reported using a broad range of tools and resources to do so. Technological advancements, as well as the emergence and rapid adoption of social media, have shifted recruiting efforts to online platforms. This stands in contrast to the previous labour market information report published in 2011, where employee referrals were the most common recruitment method. The table on the right shows the prevalence of various recruitment methods within the sector.